By Jenny Jones

With high inflation and the Federal Reserve’s efforts to temper it through multiple interest rate hikes, much speculation has swirled around whether the U.S. economy already has or soon will spiral into recession. And whether it is inevitable or a so-called soft landing is in store, economists agree that the architecture, engineering, and construction industry will see a slowdown, with some sectors faring better than others this year.

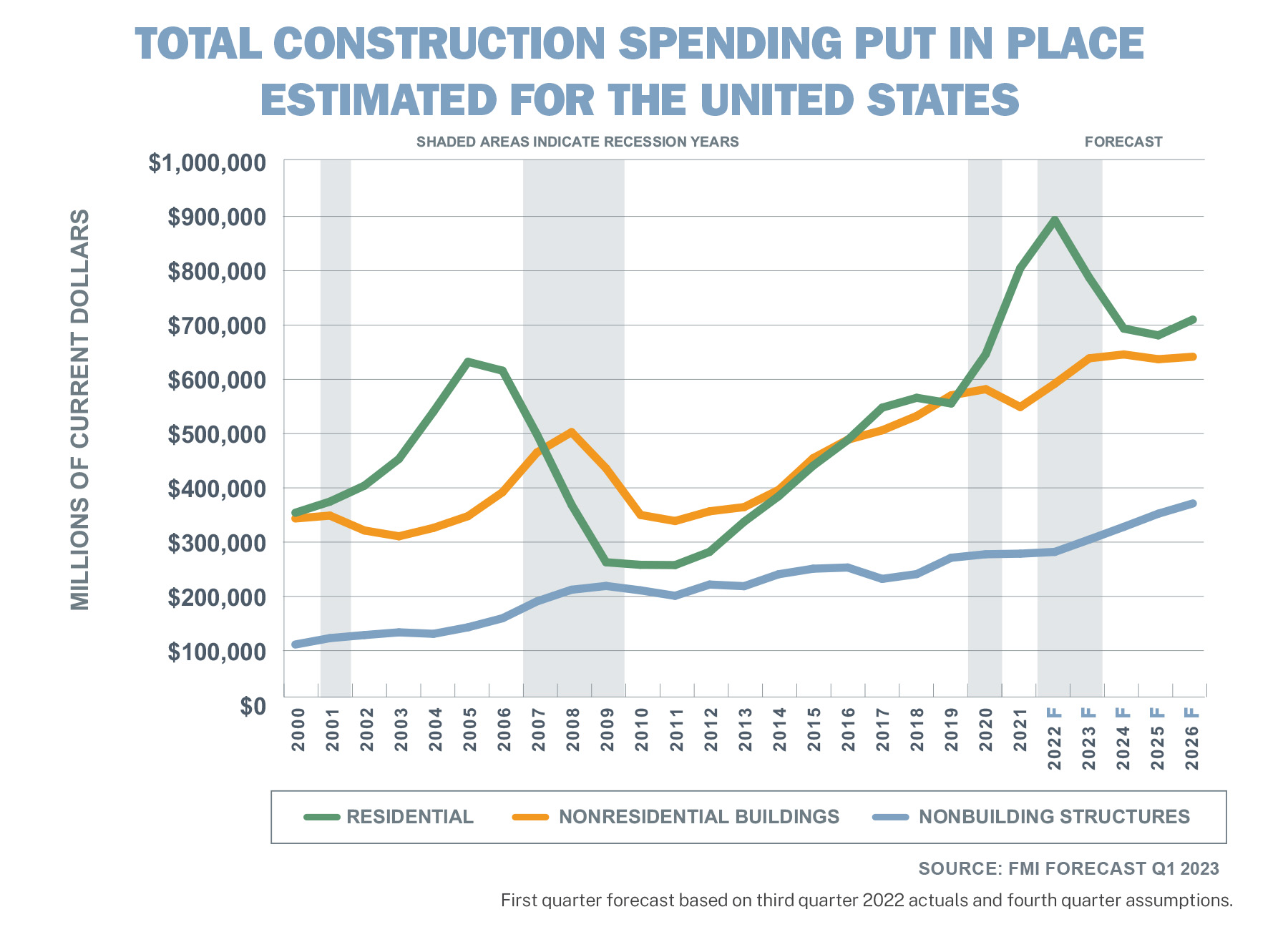

In its 2023 North American Engineering and Construction Industry Overview: First Quarter Edition, FMI Corp., a consulting and investment banking company, notes that many architecture, engineering, and construction firms ended 2022 with record backlogs, earnings, and revenue. In fact, the U.S. Census Bureau reports that construction spending was up 10.6% in 2022 compared with the previous year, rising from just over $1.6 trillion to almost $1.8 trillion.

But those gains are not expected to last. FMI predicts that while much of the industry — including infrastructure and manufacturing — will see continued growth, overall construction spending will decline 2% in 2023 as the Fed’s interest rate hikes cool the economy at large.

“At the heart of it, the construction sector is an interest-rate sensitive portion of the economy,” says Richard Branch, chief economist for Dodge Construction Network, which published the Construction Outlook 2023.

“It hasn’t been just one interest rate hike from the Fed; it’s been a cumulative response, and rate hike after rate hike after rate hike does over time start to suppress overall economic activity, which is exactly what the Fed is trying to do to get inflation down,” Branch explains.

Residential bellwether

The sector most impacted by interest rates is residential. In its report, FMI predicts that single-family residential construction spending peaked in the summer of 2022 — before the Fed introduced significant rate increases — and that it will decline at least 20% this year with a continued downward trajectory into 2025.

FMI chief economist Brian Strawberry explains that high interest rates are contributing to home affordability issues, which means reduced demand for new construction. “Even though pricing on existing and new homes has slowed down considerably in recent months, you’re looking at a much higher payment than you were even a year or two ago because of rising interest rates,” he says.

The impact is evident. According to Kermit Baker, chief economist for the American Institute of Architects, which administers the Consensus Construction Forecast, the seasonally adjusted annual rate shows that single-family starts were up at 1.8 million in April 2022 but down to 1.3 million by early 2023 — a decline of almost 30%.

While the decrease is notable, Baker is optimistic that it will be short-lived. “I’m guessing we’re probably pretty close to the bottom right now in terms of level of housing production, or we will be over the next few months,” he says.

“Mortgage rates are starting to come back down as investors feel that inflation is more under control, and we still see strong job growth numbers. These are very accurate leading indicators for homebuilding activity, so I think it will be a fairly mild downturn for housing,” notes Baker.

While single-family residential construction slows, the multifamily sector is expected to remain stable this year with a chance of modest growth. In its Construction Outlook, Dodge projects that multifamily residential spending will rise 1% to $153 billion as starts drop 9%. FMI forecasts higher gains in the multifamily sector this year, with spending up 8% before an 11% decline in 2024 and stabilization in 2026.

“Demand for multifamily construction is expected to be resilient over the forecast period due to current monetary policies, high purchasing costs, and a weakened consumer base,” the FMI report states. “Market dynamics that include higher borrowing, maintenance, and other living expenses will create a temporary period that will motivate would-be first-time buyers into rentals for longer until home prices are better aligned with incomes.”

Commercial forecast mixed

Like residential, commercial construction is heavily impacted by the overall economy. Dodge projects a 3% dip in commercial construction spending and a 15% decrease in square footage, both fueled by reductions in retail, office, lodging, and warehousing. “When the economy slows down, consumers spend less, and that means less demand for retail space,” Branch explains.

“The same goes for travel. We travel less, and there’s less demand for hotels. And then thinking about the office sector, as the economy slows down, that impacts the number of office workers hired, so it suppresses demand for office construction, which is already facing the constraint of more hybrid and remote work,” Branch says.

While Dodge expects a slowdown in warehousing due to overbuild, FMI projects that warehouse and distribution center construction will continue to bolster the commercial sector, which it estimates will see a 7% uptick in spending this year before an 11% decrease in 2024.

“E-commerce as a share of sales bottomed at the beginning of 2022 and grew through the third quarter to nearly 15% share, now exceeding year-over-year 2021 levels and pre-COVID 2020 levels at just under 12% share,” the FMI report states.

“As a result, construction spending within the commercial space will remain largely driven by warehouse and distribution centers, which now represent more than 50% of annual segment spending,” per the FMI report.

A bright spot that Dodge foresees is data center construction, according to Branch. “Data center construction has been a key pillar of support for construction since the start of the pandemic as the demand for more cloud space and more streaming services has taken off, driving increased demand for data center properties,” he explains.

“I expect demand for cloud space to keep growing more and more, so data center construction will take on an even greater share of the market,” Branch states.

Still, Branch notes, data center construction will likely remain clustered in specific areas of the country — those along the nation’s internet backbone and with strong power supplies that include renewables. “When we look at the areas of the country that are experiencing the most growth because of data centers, it’s really (confined) to four places: Texas, Illinois, Virginia, and parts of the upper Midwest, like Nebraska,” he says.

Legislation propels gains

With residential slowing and commercial mixed, the manufacturing and infrastructure sectors are expected to also help buoy the AEC industry this year, thanks largely to federal legislation. In manufacturing, FMI predicts a 20% increase in spending to $119 billion due to the CHIPS and Science Act, which allocates approximately $280 billion in federal funding for domestic semiconductor manufacturing, and Executive Order 14005 (Ensuring the Future Is Made in All of America by All of America’s Workers), which authorizes the Made in America Office to spend federal tax money on American-made goods.

Recent supply chain issues are also driving increased manufacturing demand, according to the FMI report.

“In industrial, there were all the supply chain snarls, and a lot of companies found out the real limitations to globalism,” Baker says. “Now, there is this surge to bring some production back onshore, so that we can cope with these inevitable problems that we’ve seen materialize during the pandemic. I don’t think we’re going to reverse the decadeslong trend of outsourcing a lot of manufacturing, but I do think there’s going to be a little bit of a correction, and that’s why we’re going to see this surge in manufacturing activity.”

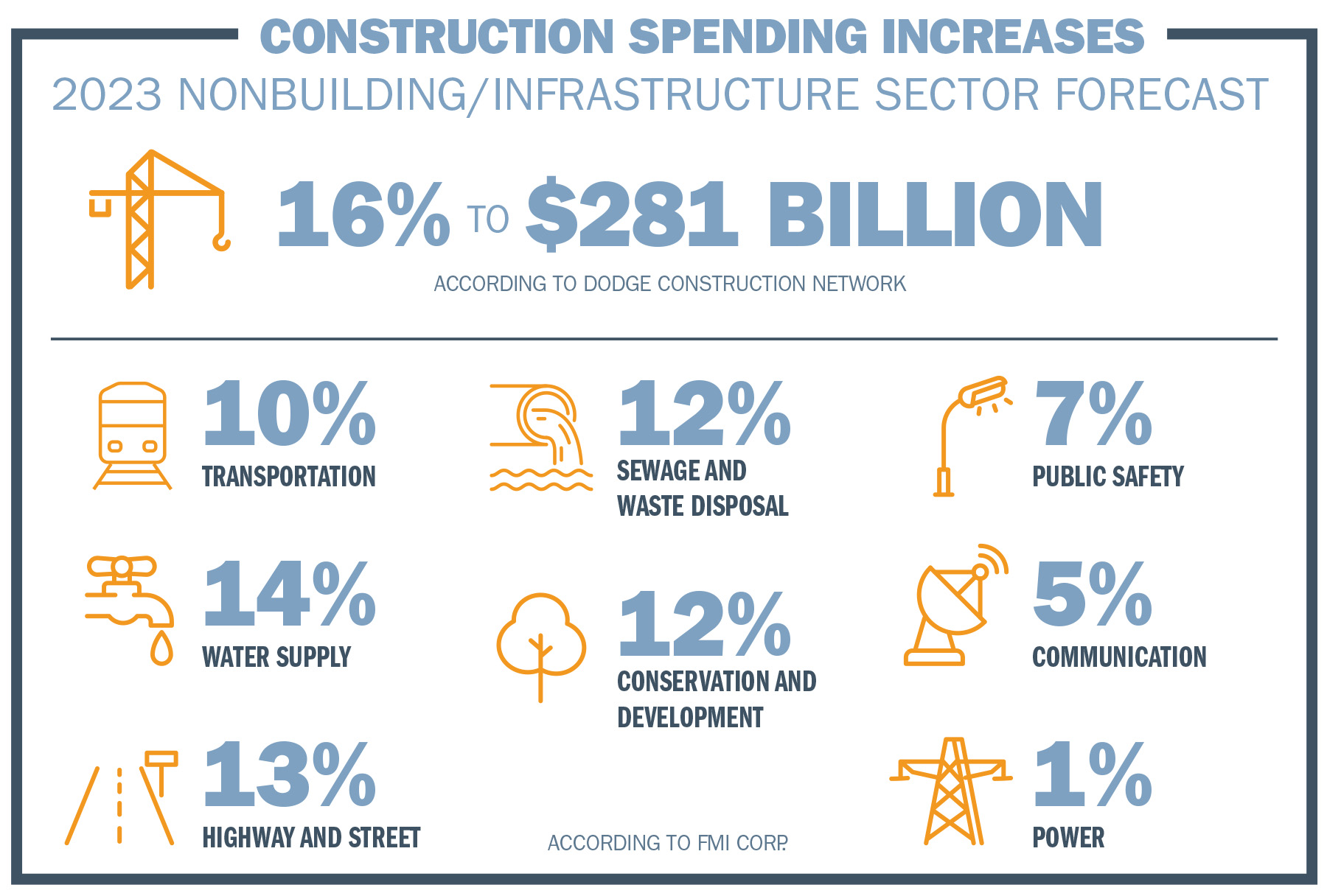

When it comes to the nonbuilding/infrastructure sector, Dodge predicts construction will increase 16% in 2023 to $281 billion, with all segments benefiting from the $1.2 trillion Infrastructure Investment and Jobs Act that Congress passed in 2021. FMI projects spending increases of 10% in transportation, 14% in water supply, 13% in highway and street, 12% in sewage and waste disposal, 12% in conservation and development, 7% in public safety, 5% in communication, and 1% in power this year.

“The timing of the IIJA funds did not hit 2022 as expected, but they did begin showing up late in the year,” Strawberry explains. “We expect another one or two very strong years as those funds are tied to projects and spending gets underway, particularly in 2023.”

Backlog not immune

While economic forecasting in the AEC industry primarily focuses on project starts and spending, backlog is also a factor. According to Associated Builders and Contractors’ Construction Backlog Indicator, backlog declined 0.2 months to 9.0 months in January. Although backlog remains elevated compared with historical standards, the dip could be an ominous sign of things to come, notes ABC chief economist Anirban Basu.

“ABC has projected for months that recession is on the horizon, perhaps later this year,” Basu says. “If economic weakness grips the economy, project planning diminishes, eventually translating into fewer future opportunities. Eventually, backlog is whittled away. While publicly financed construction is set to remain strong, many contractors are indicating potential weakness in 2024. That’s consistent with ABC’s forecast.”

Firms could not only see their backlogs dwindle as economic conditions drive down starts, but they could also see projects in the pipeline delayed. “What we’ve seen in prior cycles is that backlogs are not as stable as we might hope they would be,” Baker explains. “We could have eight or 10 months of backlog, and suddenly, we could get a whole slew of project cancellations, and before we know it, our backlog has shrunk to three or four months.”

With that in mind, Baker recommends that AEC firms keep a close eye on projects in the pipeline to ensure they keep moving forward. “What the entire AEC industry could do is monitor those project-level activities a little more closely in these uncertain times to make sure that everyone still has the same image of what that project is going to look like, and no one is getting cold feet as economic conditions begin to change,” he says.

Even on balance

As economic uncertainty looms and recession talk continues, many in the AEC industry could find themselves thinking back to the Great Recession, when, according to the U.S. Bureau of Labor Statistics, the construction industry shed 1.5 million jobs between 2007 and 2009. But even if the economy slides into recession this year, Branch is confident it will be nothing like before.

“We’re walking a tightrope here to be sure, but this will be nothing like what we saw during the Great Recession,” he says. “There will be some sectors of the industry that feel recessionary. That would be residential and income property types. But the public building types, manufacturing and infrastructure, should continue to grow. So, on balance, the construction sector should come out pretty even this year.”

Jenny Jones is an award-winning freelance writer based in northern Virginia. She has more than 20 years of editorial experience and specializes in making complex subjects clear and engaging.

This article first appeared in the May/June 2023 print issue of Civil Engineering as “An Uneven Slowdown.”